The Great Settlement Heist: Wall Street’s Colonization of Crypto Infrastructure

The 12 basis point fee war on Bitcoin ETFs was never the main event; it was the loss leader. While retail and macro investors focused on the approval of spot ETFs in early 2024, a far more structural shift began in the back offices of BNY Mellon, State Street, and Citi. The metric that matters is not Assets Under Management (AUM), but Assets Under Custody (AUC) and Settlement Velocity.

When a bank moves a billion dollars of value through a legacy wire system, it involves T+2 settlement, counterparty risk, and trapped capital costs. Moving that same value across a proprietary, permissioned blockchain ledger reduces settlement to T+0 and frees up liquidity almost instantly. This efficiency gain—worth billions in annual capital savings—is the driver behind TradFi Infrastructure Colonization. We are witnessing a strategic pivot where banks are no longer content to simply offer price exposure to crypto; they are seizing control of the validation and settlement rails themselves.

The Pivot from Price Exposure to Plumbing Control

The narrative that institutions want to "adopt" public blockchains is fundamentally flawed. Institutions want to co-opt the technology to upgrade their internal plumbing. The profit center is shifting from the trading desk (spreads and fees) to the custody stack, where the ownership of the ledger record equates to the ownership of the asset itself.

Why Settlement Volume Eclipses Management Fees

ETF management fees are a volume game with race-to-the-bottom pricing. In contrast, the settlement layer captures value on every movement of capital. By building proprietary settlement networks, banks can charge for the utility of instant finality while eliminating the fees currently paid to public chain validators (miners/stakers).

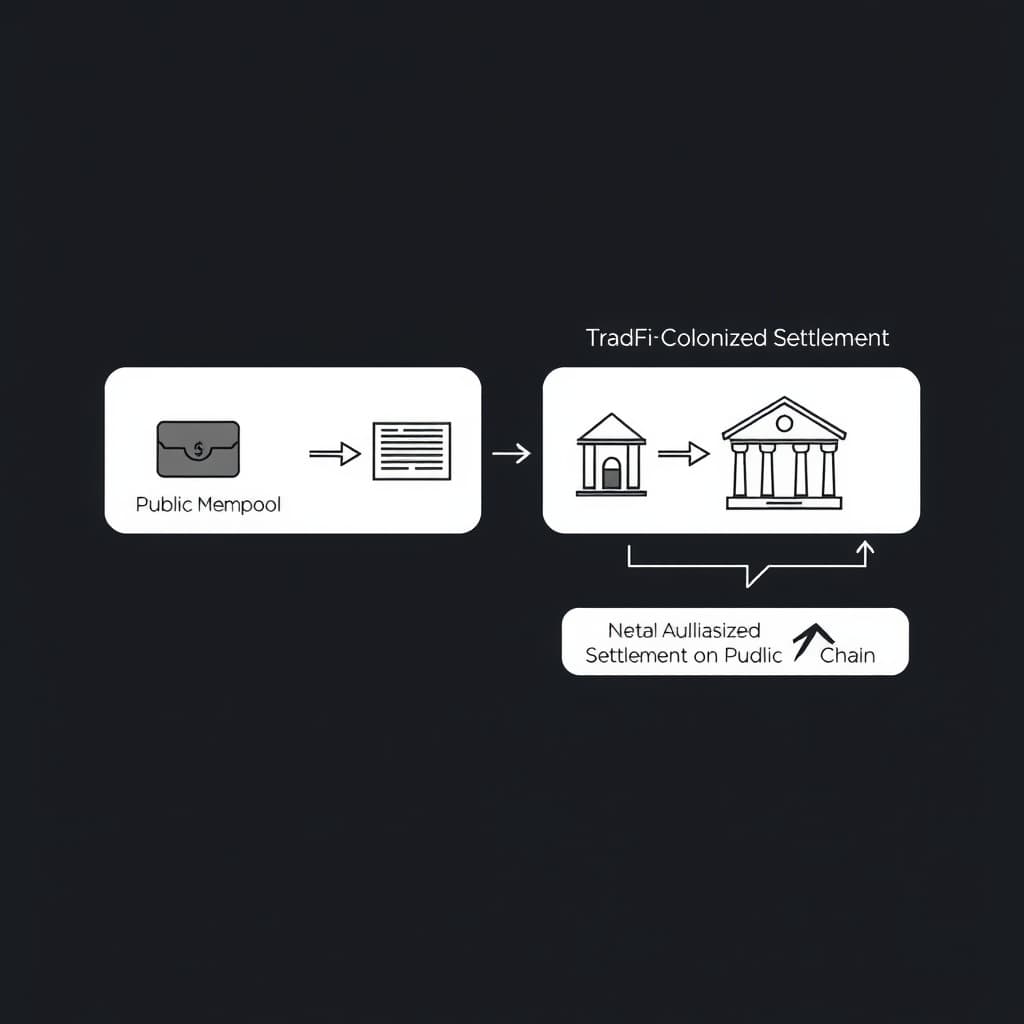

Consider the economics of a "Colonized Settlement" model:

- Internalization: Transactions between clients of the same bank (or bank consortium) never touch the public mainnet. They settle on a private ledger.

- Netting: Only the net difference between institutions settles on the public blockchain (e.g., Ethereum) at the end of a trading window.

- Result: The bank captures the transaction fee that would have gone to the public network, while the public chain is relegated to a low-volume, high-value settlement anchor.

Moving the Profit Center to the Back Office

The "custody stack" is currently fragmented. A crypto-native hedge fund might use Fireblocks for MPC wallets, Coinbase for execution, and a separate administrator for reporting. Banks are rebuilding this as a vertically integrated service.

Weaponizing the OCC Charter Against Crypto Natives

The Office of the Comptroller of the Currency (OCC) holds the keys to the kingdom: Federal Preemption. This is the regulatory moat that crypto-native firms, regardless of their technical superiority, struggle to cross.

Leveraging Federal Preemption

For a fintech or crypto exchange to operate nationally in the US, they must navigate a "hellscape" of 49 distinct state money transmitter licenses (MTLs), each with different reporting requirements and capital controls. A federally chartered national bank bypasses this entirely. State banking regulators cannot interfere with the core banking functions of a national bank.

By obtaining or utilizing existing OCC charters to offer crypto custody, Wall Street giants effectively commoditize the regulatory compliance that crypto natives spent a decade building. They don't need to innovate on the tech; they just need to apply their federal shield to the existing infrastructure.

The "Qualified Custodian" Stranglehold

The SEC’s proposed amendments to the Custody Rule (Rule 206(4)-2) are the tactical nuke in this strategy. The proposal aims to redefine "Qualified Custodian" in a way that makes it exceptionally difficult for state-chartered trusts and non-bank entities to comply.

If these rules are finalized as currently written, registered investment advisers (RIAs)—which include most crypto hedge funds—will be legally mandated to store their assets with a Qualified Custodian. If crypto-native firms cannot meet the capital or segregation requirements, the business defaults to the banks. This is not a market victory; it is a regulatory capture of the customer base.

The Citi and Morgan Stanley Blueprint: Tokenized Liabilities

The most significant technical shift is the move away from stablecoins (like USDC or USDT) toward Tokenized Deposits. This distinction is critical for risk managers and treasurers.

Replacing Stablecoins with Regulated Liabilities

A stablecoin is effectively a bearer instrument representing a claim on a reserve. A tokenized deposit is the bank deposit, just recorded on a different ledger.

- Risk Profile: Tokenized deposits fall under existing deposit insurance schemes and bank capital requirements.

- Operational Reality: Large institutions prefer trading liabilities (which they understand) over bearer assets (which introduce novel theft risks).

Citi’s "Regulated Liability Network" (RLN) proof-of-concept is the blueprint here. It envisions a shared ledger where central bank money, commercial bank money, and electronic money exist on the same partition. This allows for atomic settlement without ever leaving the regulated banking perimeter.

Building "Walled Garden" Ledgers

These tokenized deposits will likely not circulate freely on Uniswap. They will exist within "Walled Gardens"—permissioned forks of public chains or entirely private subnets (like an Avalanche Subnet or a private Ethereum L2).

In this environment, smart contracts govern the flow of funds, but the "allow list" for who can interact with those contracts is controlled by the bank’s compliance department. This solves the "sanctioned wallet" problem for institutions: you literally cannot send money to a bad actor because their address cannot exist on the private ledger.

The Bifurcation of Liquidity: 2026 and Beyond

We are heading toward a bifurcated liquidity landscape. The "unitary" view of the blockchain universe—where everyone shares the same mempool—is ending for institutional capital.

White-Listed DeFi vs. Dark Forest DeFi

By 2026, we will see the emergence of "White-Listed DeFi". These will be liquidity pools (AMMs, lending markets) that are clones of Aave or Uniswap but deployed on permissioned bank chains.

- Access: Only KYC’d wallets from participating banks can enter.

- Yield: Likely lower than public DeFi due to lower risk and compliance costs, but higher than traditional treasuries.

- Collateral: Real World Assets (tokenized treasuries, corporate bonds) will dominate these pools, not volatile crypto assets.

The Acquisition Spree

Banks are historically bad at building software. They will not build these stacks from scratch. Instead, we should anticipate an acquisition spree targeting "crypto infrastructure" firms—not for their tokens or user bases, but for their engineering teams and custody tech. The era of the "crypto mullet" (fintech front, crypto back) is ending. Wall Street is bringing the back office in-house.

Falsifiable Claim & Indicators

Claim: By Q4 2026, over 50% of institutional "on-chain" transaction volume (defined as transfers >$1M) will occur on permissioned Layer-2s or private bank consortium ledgers, rather than public mainnets (Ethereum/Solana).

Watch these indicators to confirm or refute:- The "Gas" Metric: If institutional AUM in crypto rises but Ethereum mainnet gas usage from institutional wallets flatlines or drops, the activity has moved to private layers.

- The RLN Pilot: If the Regulated Liability Network moves from "Proof of Concept" to "Production" with more than 3 major US banks, the colonization is active.

- Stablecoin Market Cap vs. Deposit Token Volume: A divergence where USDC/USDT market cap stabilizes while "Bank Deposit Tokens" (tracked by bank reporting) explode.

What Would Change My Mind

Two specific scenarios would derail this thesis. First, if Zero-Knowledge (ZK) privacy technology on public chains matures rapidly enough to satisfy strict institutional compliance and privacy requirements (e.g., concealing trade intent and counterparty identity perfectly), banks might opt to use public rails directly to save on infrastructure costs. Second, a draconian continuation of SAB 121 (Staff Accounting Bulletin 121) by the SEC, which effectively makes it too expensive for banks to hold crypto assets on their balance sheets. If this rule is not repealed or modified, banks may be forced to abandon custody entirely, leaving the field open to crypto-native custodians like Coinbase and Anchorage.

The New Settlement Layer

The battle for Bitcoin and Ethereum ETF approval was merely the opening skirmish. The real conquest is the infrastructure. For the last decade, crypto proponents believed they were building a parallel financial system. In reality, they were beta-testing the R&D department for the world's largest banks. The next phase isn't about price; it's about who validates the transaction. If Wall Street succeeds, public blockchains will become the deep-layer settlement anchors for a new, highly gated banking network.

FAQ

Why are banks building their own infrastructure instead of using Coinbase or Anchorage? Banks require absolute control over counterparty risk and regulatory compliance. Relying on third-party crypto natives introduces "vendor risk" that the OCC and Federal Reserve explicitly warn against. Furthermore, owning the ledger allows banks to capture the settlement fees rather than paying them to a third party.

Does this mean the end of public permissionless blockchains? No, but it likely relegates them to a base settlement layer for institutions. High-velocity transaction volume will move to proprietary, permissioned L2s controlled by major banks, while public chains will serve as the final "court of arbitration" for net settlement and for the retail/permissionless economy.

Sources

- Office of the Comptroller of the Currency (OCC) - Interpretive Letter #1170

- SEC Proposed Rule: Safeguarding Advisory Client Assets

- Bank for International Settlements (BIS) - The Unified Ledger

- [Citigroup - Money, Tokens, and Games](https://ir.citi.com/gps/x5%2BFm%2B%2Fj%2B%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F%2F

Loading comments...

Related

View all →

Crypto

Enterprise Stablecoin Inflection: Why Corporate Finance is Nearing its 'ChatGPT Moment'

March 28, 2026

...