Sovereign-Rail Integration: When Crypto Exchanges Become Settlement Banks

During the regional banking crisis of 2023, the collapse of Silvergate and Signature Bank didn't just freeze funds; it severed the primary API bridges between the crypto economy and the US dollar. The industry learned a hard lesson in infrastructure dependency: relying on commercial intermediaries for fiat settlement introduces a single point of failure that operates on banking hours, not blockchain hours.

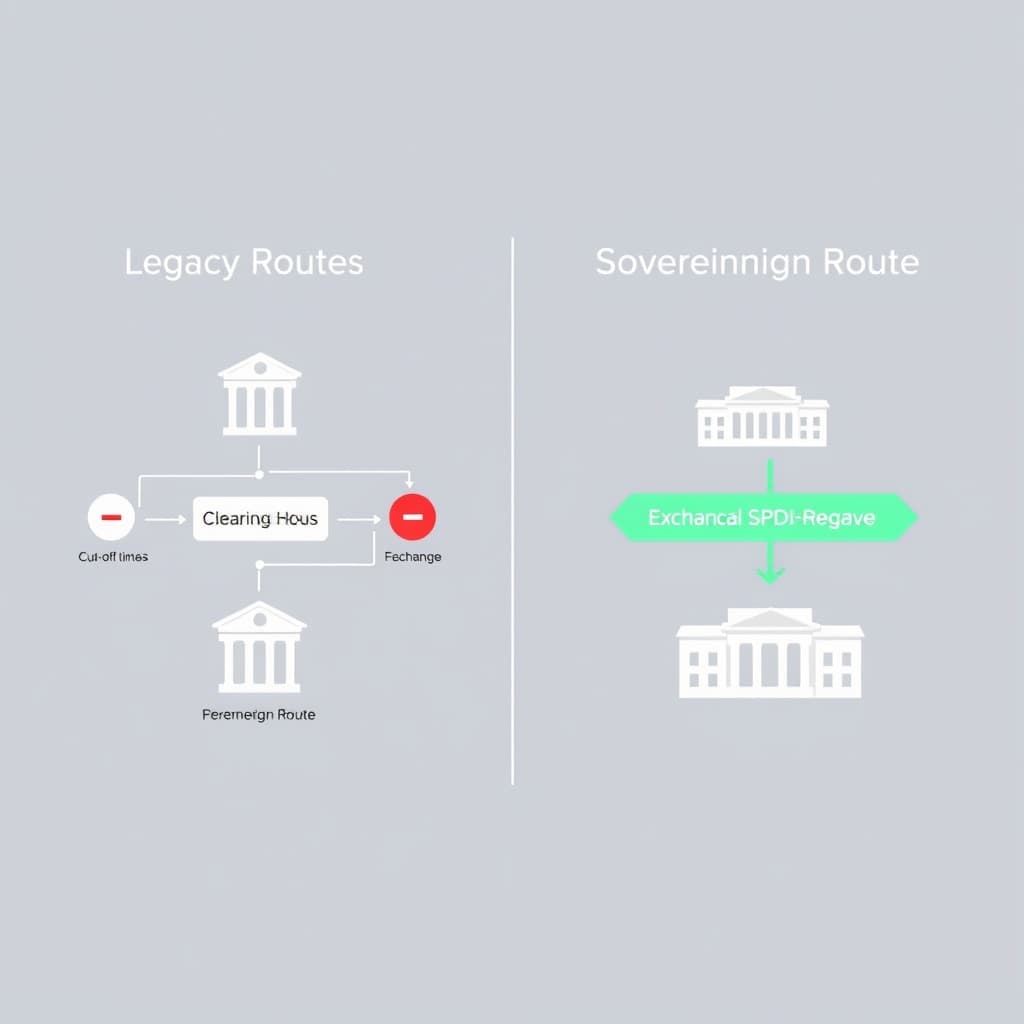

The recent approval of Kraken to access the Federal Reserve’s Core Payment System marks the end of the "client-bank" era and the beginning of the "peer-bank" model. This is not merely a regulatory win; it is a fundamental re-architecture of how capital moves between digital assets and sovereign fiat. By securing a Master Account, an exchange transitions from a merchant relying on third-party permission to a sovereign node with direct access to the national ledger.

Anatomy of a Sovereign Node: How Direct Clearing Works

For over a decade, crypto exchanges operated as second-class citizens in the financial hierarchy, nesting their operations within commercial banks that acted as gatekeepers. Sovereign-Rail Integration removes this nesting.

Bypassing the Correspondent Banking Layer

A Federal Reserve Master Account is effectively a direct row in the central bank's ledger. When an exchange possesses this, it no longer needs a commercial bank to settle transactions on its behalf.

In the legacy model, a wire transfer from a user travels through a chain of correspondent banks, each adding latency, fees, and compliance friction. In the sovereign model, the exchange initiates settlement directly via the FedWire Securities Service or the FedNow Service. This flattens the topology of the network. The exchange is no longer asking a bank to move money; it is instructing the central bank to update the ledger.

Technical Integration: FedWire vs. FedNow

Direct access requires distinct technical implementations for two different liquidity needs:

- FedWire (High-Value, RTGS): Used for institutional settlement and large-scale arbitrage. This is a Real-Time Gross Settlement system where transactions are final and irrevocable immediately upon execution.

- FedNow (Instant, 24/7): This is the critical rail for retail flows. Unlike FedWire, which closes on weekends and holidays, FedNow offers continuous availability, aligning fiat settlement times with the 24/7 nature of crypto markets.

For a CTO or Head of Payments, the integration challenge shifts from managing bank APIs (which vary by institution) to maintaining strict ISO 20022 compliance directly with the Fed.

The Wyoming SPDI Blueprint and the Kraken Precedent

The vehicle delivering this access is not a standard commercial banking charter, but the Special Purpose Depository Institution (SPDI) framework pioneered by Wyoming. This structure was specifically engineered to bridge the gap between digital asset custody and federal payment rails.

Understanding the SPDI Framework

The SPDI is a "narrow bank." Unlike traditional banks that lend out deposits to generate interest (fractional reserve banking), an SPDI is prohibited from lending. It must hold 100% of customer fiat deposits in liquid, high-quality assets—typically cash at the Fed or short-term T-bills.

This creates a unique value proposition:

- For the Regulator: It eliminates the risk of a bank run causing a solvency crisis. The money is always there.

- For the Exchange: It trades the ability to earn interest on loans for the privilege of direct access to payment rails.

Regulatory Moats as Infrastructure

Kraken’s utilization of this charter demonstrates that the barrier to entry for Sovereign-Rail Integration is capital efficiency, not just compliance. Maintaining a 1:1 reserve ratio requires a business model that does not rely on net interest margin (NIM). The exchange must generate revenue purely from transaction fees and custody services, proving that the integration is a utility play, not a lending play.

De-risking the Stack: Removing the Commercial Bank Failure Point

The strategic value of direct Fed access is best understood by analyzing the failure modes of the previous cycle. When Silicon Valley Bank failed, the risk wasn't that the assets were fake; the risk was duration mismatch—the bank had invested short-term deposits in long-term bonds that lost value.

Isolating Fiat Custody

By integrating directly as a sovereign node (or SPDI), an exchange decouples its fiat custody from the lending risks of the commercial banking sector.

Lessons from the 2023 Crisis

The 2023 regional banking crisis highlighted that "crypto contagion" often flows the other way—from traditional finance to crypto. Stablecoin issuers and exchanges were nearly de-pegged not because their tech failed, but because their commercial banks failed. Sovereign integration creates a firewall. Even if the broader commercial banking sector suffers a liquidity crunch, an exchange with a Master Account and full reserves remains operational.

Institutional Velocity: FedNow and the 24/7 Liquidity Loop

The final piece of the integration puzzle is velocity. Institutional capital efficiency is currently throttled by the mismatch between blockchain speed (seconds) and wire speed (days).

Real-Time Gross Settlement (RTGS) Meets Crypto

With FedNow integration, the concept of "pre-funding" an account changes. Traders no longer need to park millions in dormant capital on an exchange over the weekend "just in case" volatility hits.

Funds can be deployed from an external fiat account to the exchange, executed on-chain, and settled back to fiat in minutes, regardless of whether it is Sunday at 3:00 AM. This collapses the arbitrage windows between spot and futures markets and significantly reduces the cost of capital for market makers.

The Convergence of Stablecoins and Sovereign Rails

This integration forces a re-evaluation of stablecoins. If a user can hold fiat in a government-insured (or fully reserved) environment and move it instantly 24/7, the utility of a private stablecoin for domestic transfer diminishes. Stablecoins remain superior for cross-border flows and DeFi composability, but for domestic USD settlement, a direct-fed exchange acts as a programmable dollar interface.

Map of Incentives: Who Wins and Loses

Understanding this shift requires looking at the incentives of the major players involved in the transition to sovereign rails.

-

The Winners:

- Exchanges: Gain vertical integration, reduced fees (no middleman bank), and immunity from "de-banking."

- High-Frequency Traders: Gain capital efficiency; no need to trap liquidity on exchanges over weekends.

- Regulators: Gain direct visibility into flows without relying on commercial bank SARs (Suspicious Activity Reports).

-

The Losers:

- Tier 2/3 Commercial Banks: Lose the massive non-interest-bearing deposit float that crypto exchanges previously provided.

- Payment Processors: Third-party gateways become redundant if the exchange connects directly to the Fed.

Conclusion

The approval of direct Fed access for crypto entities validates the sector not as a speculative casino, but as a modernization of financial infrastructure. By removing the commercial banking layer, exchanges reduce systemic risk and align fiat settlement speed with blockchain realities. As settlement latency collapses to zero, the functional distinction between a crypto exchange and a neo-bank will effectively vanish, leaving only the question of which asset class—digital or analog—the user chooses to hold.

FAQ

What is the primary benefit of Sovereign-Rail Integration for traders? It eliminates the T+1 or T+2 settlement delays associated with commercial bank wires. This allows for near-instant fiat deployment and withdrawal directly through the Federal Reserve system, even on weekends and holidays via FedNow.

Does direct Fed access guarantee deposit insurance? Not necessarily. While it grants access to clearing rails, Special Purpose Depository Institutions (SPDIs) operate under a full-reserve model. Because they do not lend money, they often do not carry FDIC insurance, but instead rely on the safety of holding 100% liquid assets to guarantee solvency.

How does this impact stablecoins like USDC or USDT? It creates competition for domestic transfers. If an exchange can offer instant, 24/7 USD movement via FedNow, the need to convert to a stablecoin solely for speed or weekend liquidity diminishes within the US domestic market.

Sources

Loading comments...

Related

View all →

Crypto

Enterprise Stablecoin Inflection: Why Corporate Finance is Nearing its 'ChatGPT Moment'

March 28, 2026

...