Asymmetric Chokepoint Taxation: How Hormuz Transit Fees Are Rewiring Global Energy Markets

Asymmetric Chokepoint Taxation: How Hormuz Transit Fees Are Rewiring Global Energy Markets

Routing a standard Very Large Crude Carrier (VLCC) through the Strait of Hormuz in late March 2026 now carries a staggering financial penalty of up to $14 million per voyage. This is not a reflection of fuel costs, labor, or standard port tariffs. Instead, it represents a calculated financial extraction model imposed by Iranian authorities, heavily compounded by soaring war-risk insurance premiums. Applying quantitative risk modeling to maritime logistics reveals a chilling reality: this dynamic has permanently altered the baseline cost of global energy. By leveraging geographic control to extract exorbitant capital from transiting vessels, sovereign actors are executing a strategy of asymmetric chokepoint taxation.

The Economics of Geopolitical Extortion at Sea

The tactical doctrine of maritime conflict has pivoted away from the absolute denial of transit. Total blockades invite immediate, overwhelming military retaliation. Sovereign actors have learned that financial friction is far more sustainable than kinetic warfare.

Shifting from Physical Blockades to Toll Booths

Historically, the threat in the Persian Gulf was a binary closure of the waterway. Today, the mechanism is nuanced. Following the escalation of the US-Iran conflict in late February 2026, Iranian forces established what they term a "safe corridor" requiring visual verification and approval. Rather than sinking every ship, the coastal authority creates an environment of acute, localized risk that terrifies the actuaries in London.

By selectively targeting vessels with perceived US, UK, or Israeli affiliations, the authority forces shipowners into a highly restrictive compliance framework. The threat of seizure or drone strikes acts as the enforcement mechanism for this new toll booth. The result is a shadow tariff: operators must either pay direct transit fees for "safe passage" or absorb catastrophic insurance premiums that achieve the exact same economic degradation.

The Multi-Million-Dollar Transit Fee Mechanism

The actual taxation occurs at the intersection of sovereign extortion and actuarial science. When the Joint War Committee (JWC) in London designates a region as a high-risk Listed Area, standard hull insurance policies are voided. Shipowners must purchase Additional War Risk Premium (AWRP) coverage.

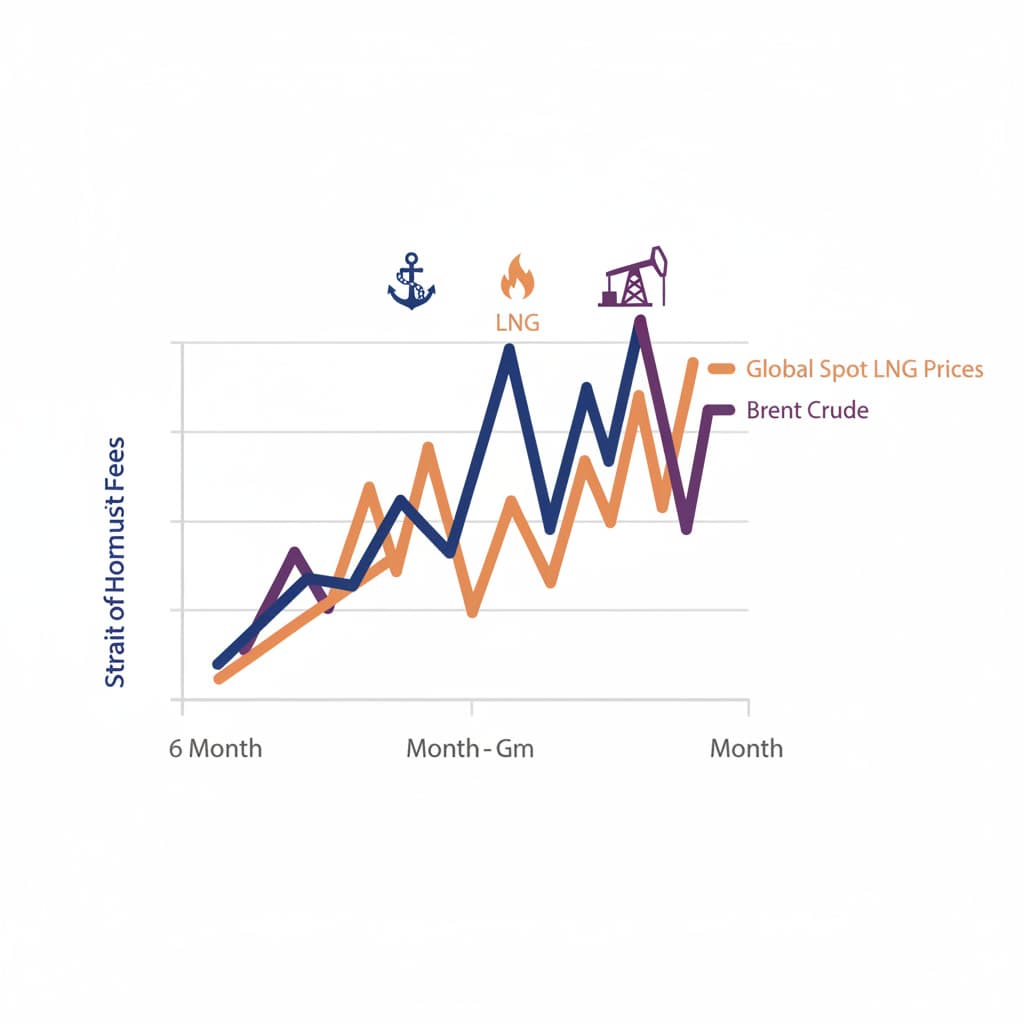

Before the February 2026 strikes, transiting the Gulf cost roughly 0.125% to 0.4% of a vessel's hull value. By mid-March, quotes for high-risk vessels surged to between 5% and 10%. For a modern VLCC valued at $138 million, the transit penalty scales to roughly $10 million to $14 million per voyage. This capital extraction flows either directly to risk underwriters or, indirectly, to the sovereign actors demanding off-book payments to guarantee safe passage. This is the textbook definition of asymmetric chokepoint taxation.

Immediate Fallout on Global Energy Pricing

The imposition of these multi-million-dollar fees does not merely compress shipping margins. It fundamentally re-prices the underlying commodities. Because 20% of global seaborne oil and roughly 20% of global liquefied natural gas (LNG) pass through this 21-mile-wide corridor,, the macro-level impact is immediate and structural.

Establishing Brent Crude's New Baseline Premium

Brent crude surged nearly 50% to $112 a barrel following the initial outbreak of hostilities. While spot prices often spike during geopolitical crises, the sustained elevation is driven by the new transit arithmetic. A $14 million transit fee amortized across a VLCC's two-million-barrel cargo adds exactly $7 to the break-even cost of every barrel,.

This $7 per barrel is the asymmetric tax. It establishes a new baseline premium that cannot be erased by simply increasing production in other regions. Because the global market prices at the margin, the highest-cost marginal barrel dictates the clearing price. As long as the Strait of Hormuz operates under this extortionary framework, global crude prices carry a structural floor that did not exist in 2025.

Navigating the Imminent LNG Supply Cliff

While crude oil can occasionally be rerouted through pipelines—such as the 3.5 million barrels per day of unused capacity in Saudi Arabia and the UAE—LNG relies entirely on specialized maritime transport. Qatar exports approximately 9.3 billion cubic feet per day of LNG through the Strait.

LNG markets are exponentially more sensitive to transit delays. The cryogenic nature of the cargo means continuous boil-off occurs during extended voyages or while anchored awaiting clearance. The sudden imposition of asymmetric chokepoint taxation forces LNG carriers to either absorb the massive AWRP or halt shipments entirely, creating an immediate supply cliff for primary importers like China, India, and South Korea.

Strategic Trade-Offs for Fleet Operators

The boardroom calculus for maritime logistics companies has shifted from optimizing fuel efficiency to managing existential geopolitical risk. Operators face a trilemma with no optimal solutions, forcing a rigid decision matrix.

Absorbing the Tax vs. Asset Seizure Risks

Fleet operators must decide whether to engage with the new toll system or anchor their vessels indefinitely. Complying with Iranian verification demands risks violating Western sanctions, while ignoring them invites drone strikes or asset seizure.

The following decision matrix illustrates the current operating environment for a standard VLCC operator in the Persian Gulf:

The Cost of Compliance in a Sanctioned Environment

Engaging with the asymmetric tax introduces severe legal liabilities. Paying arbitrary fees to a sanctioned entity to secure a "safe corridor" triggers immediate scrutiny from the US Treasury’s Office of Foreign Assets Control (OFAC). Fleet operators are caught between the physical reality of the chokepoint and the legal reality of the US dollar system. This regulatory friction is accelerating the bifurcation of the global shipping fleet, pushing more tonnage into the "shadow fleet" that operates entirely outside Western insurance and financial networks.

Ripple Effects Across Maritime Supply Chains

The sheer scale of capital required to underwrite these transits is draining liquidity from other segments of the maritime supply chain. The secondary effects extend far beyond the energy sector.

Insurance Underwriting and Rerouting Calculus

The Lloyd's of London insurance market remains the central nervous system for global shipping. As underwriters allocate billions in capital to cover potential hull losses in the Persian Gulf, insurance capacity for other regions tightens.

We see this manifesting in the broader container shipping market. Vessel tracking data indicates that container ships, which previously made up a significant portion of the 153 daily transits through the Strait, have essentially vanished from the corridor. The cost of insuring a $200 million container ship carrying $500 million in cargo is mathematically prohibitive under a 7.5% AWRP. Consequently, supply chains reliant on Middle Eastern petrochemicals and manufactured goods are forced into costly air freight or face total supply denial.

Technological Countermeasures in Fleet Tracking

To mitigate exposure, operators are deploying advanced technological countermeasures. Automatic Identification System (AIS) spoofing, once the exclusive domain of illicit smugglers, is being adopted by mainstream commercial operators to obscure their approach vectors into the Gulf.

These countermeasures offer diminishing returns. Sovereign actors utilize shore-based radar, satellite imagery, and drone surveillance to enforce their asymmetric taxation regardless of AIS broadcast status. The technological arms race between commercial evasion and sovereign detection heavily favors the entity controlling the geographic chokepoint.

Long-Term Market Restructuring (2026-2030)

The events of March 2026 guarantee that the global energy market will not return to its pre-conflict architecture. The realization that a sovereign actor can successfully impose an asymmetric tax on 20% of the world's oil and LNG, without triggering a full-scale naval invasion permanently alters the risk premium of Middle Eastern energy.

Accelerating the Shift to Non-Middle Eastern Energy

Capital allocation models are already adjusting. The $7 per barrel transit tax effectively acts as a subsidy for non-Middle Eastern energy production. Projects in the Atlantic Basin, deepwater Guyana, and US shale formations that were marginal at $70 a barrel become highly lucrative when the global clearing price is artificially supported by chokepoint taxation.

For LNG, the vulnerability of Qatari exports will accelerate the development of export terminals in the US Gulf Coast and East Africa. Importers in Asia cannot tolerate a supply chain where a single geopolitical actor can arbitrarily double the delivered cost of natural gas via transit extortion.

The Normalization of Sovereign Chokepoint Tolls

The most dangerous legacy of the Hormuz crisis is the precedent it sets. If asymmetric chokepoint taxation proves economically viable for Iran, other state and non-state actors controlling critical maritime geography—such as the Strait of Malacca or the Bab el-Mandeb—will adopt similar financial extraction models. The era of the "freedom of the seas," guaranteed by unquestioned Western naval hegemony, is transitioning into a fragmented system of regional toll roads.

Asymmetric chokepoint taxation transitions geopolitical risk from a temporary supply shock to a structural overhead cost. Market observers must closely monitor shipping insurance adjustments and the rapid diversification of LNG sourcing as early indicators of permanent supply chain realignment. The cost of global trade has fundamentally changed, and the toll collectors are just getting started.

FAQ

What exactly constitutes asymmetric chokepoint taxation in maritime logistics? It refers to a sovereign entity leveraging its geographic control over a critical maritime strait to impose arbitrary, unilateral financial levies on transiting commercial vessels, effectively taxing global trade without legal jurisdiction or international consensus.

How does the Strait of Hormuz fee structure affect LNG differently than crude oil? LNG carriers are highly specialized and operate on tight, continuous delivery schedules with fewer alternative routing options compared to crude oil tankers. This makes LNG markets exponentially more sensitive to transit delays, localized fees, and sudden spot price shocks.

Sources

- U.S. Energy Information Administration: World Oil Transit Chokepoints

- U.S. Energy Information Administration: About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz

- Lloyd's List: Gulf war risk premiums topping double-digit millions of dollars per trip

- The Guardian: 'Huge build-up of risk': London's centuries-old shipping industry wrestles with Iran war

- [TIME: Iran Threatens to Close Strait of Hormuz 'Completely' if Trump Attacks Power Plants](https://time.com/5759364/strait-of-hormuz-iran-

Loading comments...

Related

View all →